Over the past four decades, private equity has become a powerful, and malignant, force in our daily lives. In our May+June 2022 issue, Mother Jones investigates the vulture capitalists chewing up and spitting out American businesses, the politicians enabling them, and the everyday people fighting back. Find the full package here.

Among the 22 members of the House and Senate who reported investing in private equity last year, 10 were Republicans and 12 were Democrats. They ranked among the wealthiest members of Congress, an already elite club composed mostly of millionaires that has done little to get rid of the carried interest loophole, the quirk in federal tax law that allows a certain very select group of people—hedge fund and private equity managers—to collect their pay at a much lower tax rate than many Americans. According to money-in-politics watchdog OpenSecrets, the private equity industry spent $16.5 million lobbying Congress last year; all told, 415 of 435 members of the House and nearly every senator took money from the industry in the runup to the last election—including Congress’ five biggest private equity investors:

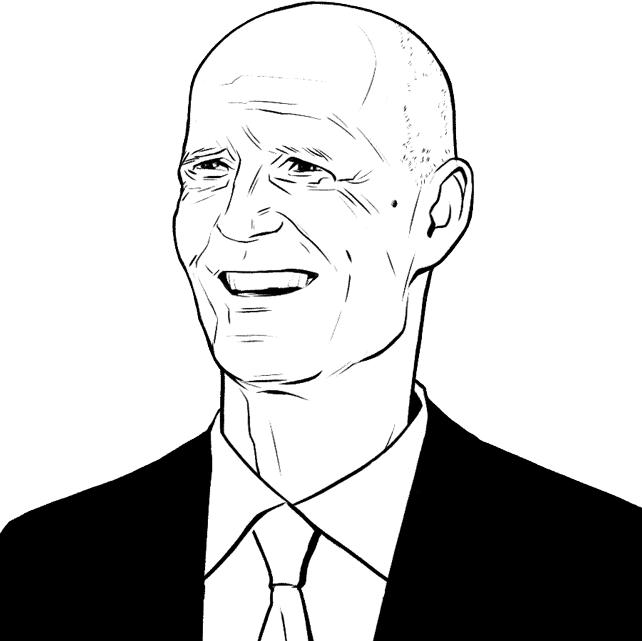

Sen. Rick Scott (R-Fla.)

The Senate’s richest member ($200 million), the former Florida governor made his fortune at the hospital chain Columbia/HCA, which the feds fined $1.7 billion for fraud and overbilling while Scott was CEO.

In February, the Scott-chaired National Republican Senatorial Committee released its “11-Point Plan to Rescue America,” a manifesto of the GOP’s grievance politics. In a throwback to Romney’s 2012 campaign, though, Scott called for the roughly 57% of households not earning enough to owe federal income taxes to pay them in the future, “to have skin in the game.”

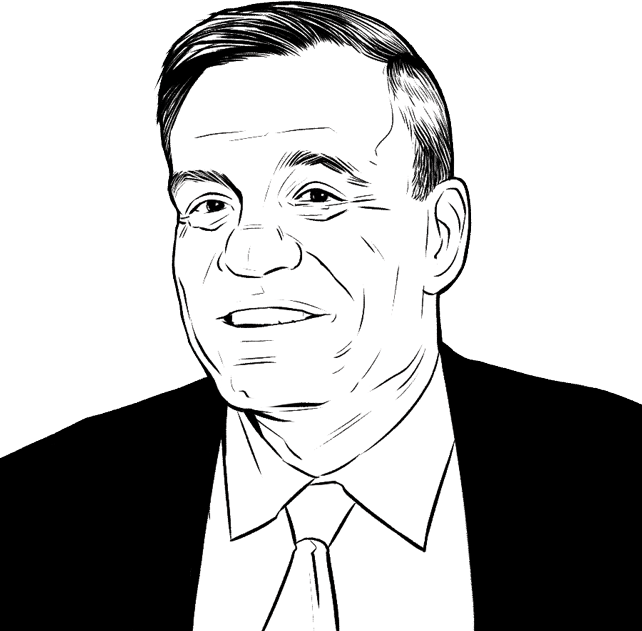

Sen. Mark Warner (D-Va.)

The third-richest senator ($94 million), Warner founded venture firm Columbia Capital in 1989. He has opposed closing the carried-interest loophole and said capitalism was “under assault” in “frankly unprecedented” ways.

In early 1986, the FCC held a lottery to divvy up the rights to build the nation’s first cellphone networks. Warner, then a young lawyer, proposed that the winners hire him to sell their collective rights as a package. They did, and Warner’s cut of the $20 million deal was some $2 million in today’s money, helping him get his start shortly thereafter with Columbia.

Rep. Suzan DelBene (D-Wash.)

A former Microsoft exec whose husband recently retired from the tech giant to work at the Department of Veterans Affairs, DelBene is the House’s eighth-wealthiest member ($52 million).

DelBene was also one of Congress’ most active stock traders in 2021: She and her husband bought more than $15 million worth of stock and sold nearly $31 million, including Microsoft shares after his retirement.

Sen. Richard Blumenthal (D-Conn.)

Connecticut’s senior senator ($85 million) married into considerable wealth: His father-in-law, Peter Malkin, was the chair of a major Manhattan real estate company and a longtime rival of Donald Trump.

In 2002, after PE firm Forstmann Little lost more than $100 million of state pension fund money, then–Connecticut Attorney General Blumenthal sued and recouped $16 million—helping him burnish his hard-charging rep.

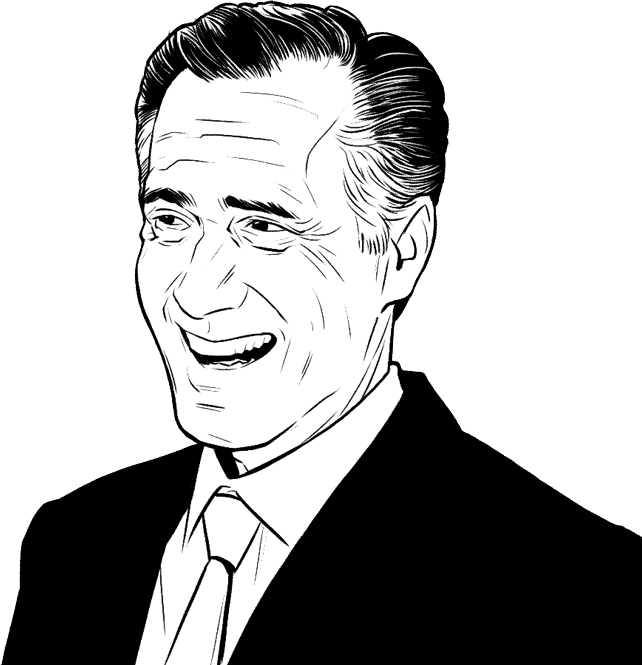

Sen. Mitt Romney (R-Utah)

Congress’ PE poster child, the fourth-richest senator (estimated net worth: $85 million) co-founded Bain Capital in 1984. In 2012, Romney’s dismissal of 47% of Americans as free-loaders helped sink his presidential campaign.

In a devastating 2012 attack ad paid for by Priorities USA, an Indiana paper-plant worker named Mike Earnest recounts how he was asked by his bosses to build a 30-foot stage—only to later realize that it was for Bain executives to announce to his co-workers that they all were being fired.