On May 4, “Ethereum Classic” popped onto the trending section of my Twitter page. I narrowed my eyes and I laughed.

This was around the time when Dogecoin was smashing previous price records, requiring mainstream business pages at places like the New York Times not only to explain cryptocurrencies to the average reader, but also to report that a meme coin—a “joke” making fun of crypto’s self-seriousness—had been taken up by Elon Musk in a wealth-scheme-cum-promotion-cycle for an appearance on Saturday Night Live. Along the way, Dogecoin was making people millionaires.

Despite that, what was going on with “Ethereum Classic” was weirder. Frankly, it was so dumb as to bring clarity.

Ethereum Classic (ETC) is the original version of Ethereum (ETH)—which is kind of like Bitcoin. Each are tokens you can digitally swap as money without having to rely on a third party, like Visa or SunTrust. ETH is a particularly popular cryptocurrency: Ashton Kutcher likes to talk about it. By market capitalization, it’s the second most valuable after Bitcoin. In addition to carrying out transactions, ETH has the added value of carrying out digital contracts. Ethereum Classic, on the other hand, does almost nothing. It was created when a hacker stole millions of dollars worth of crypto through a vulnerability in the code of a separate program. The vast majority of the Ethereum community left, created ETH and allowed the old protocol to function as a zombie blockchain. ETC became a useless ETH more prone to cyberattacks.

Yet, from the beginning of March to the beginning of May, the value of Ethereum Classic had shot up by over 1,000 percent. It jumped from about $12 a token to over $130. This isn’t entirely unprecedented during cryptocurrency boom cycles. Tokens, even ones that serve no purpose beyond being a joke like Dogecoin, explode as speculators pile in trying to get in on the next big, meaningless cash grab. But as I scrolled through tweets trying to figure out what was happening with the latest lottery, I noticed that ETC’s boom appeared to be based on a simple misunderstanding.

A pseudonymous crypto Twitter account had written in a semi-successful tweet the lie that “$ETC (Ethereum Classic) is basically the same thing as one $ETH and can be purchased on all major exchanges including #robinhood at a price that’s basically 70 times cheaper.” People, as Anthony Sassano, a prominent crypto investor and influencer on Twitter, explained, thought that they were purchasing “a cheaper version of Ethereum.” They were wrong. In fact, Ethereum Classic was like buying a Blockbuster location thinking you’re purchasing into Netflix.

More seasoned and knowledgeable crypto traders called investing in a useless protocol a “dumb” play. But as retail traders thought they were pulling off arbitrage, Ethereum Classic reached an all-time high.

Versions of this kind of financial absurdity have played out across the crypto space and the broader economy. You perhaps saw when niche markets for digital art (some of it real, some of it silly) flared; when valuations for SPACs, a way to take a company public without having a fully formed company that does anything, boomed; when various cryptocurrencies—whose projects often don’t even fully exist yet—went through the roof. Online people suddenly were—and are now—selling objects even less tangibly connected to the “real economy” than stocks. It is hard to tell what is stupid and what is genuinely important, and that’s because it doesn’t really matter: You can get rich doing it either way, as long as you can bet on some number increasing.

All this looks absurd and unprecedented—and while the methods are new, the madness is not. For the past few decades, the wealth barons have played an equally ridiculous game. Robinhood didn’t invent options trading. Putting money into cryptomarkets isn’t the first time people could invest in early-stage technologies before they were publicly listed on stock exchanges. Venture capitalists and hedge fund managers do all this professionally. Now, everyone else is finally (sort of) just catching up with them. The American Dream is not a home with a white picket fence—it’s a green ticker symbol that only goes up.

Even in a pandemic economy, the Dow is near an all-time high. Corporate profits have skyrocketed. The housing market is up. So is the computer chip market. As is the car market. If you’ve got something to sell it has probably never been worth more than it is right now.

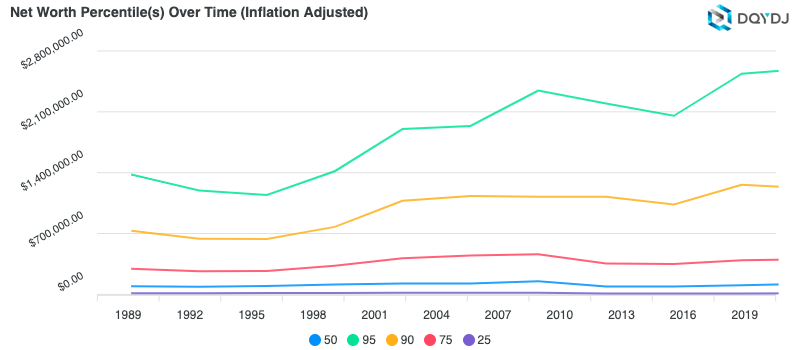

The problem is most of us do not own shit. The top 10 percent of Americans in wealth control 89 percent of Wall Street’s value. White people own 79 percent of all wealth. Homes—because of America’s history of racist redlining, a failed response to the 2009 subprime mortgage crisis that disproportionately screwed over Black Americans and other groups of color out of housing markets—are disproportionately owned by the white wealthy. A few people have a lot.

The moral question upon seeing the gap between owners and buyers, between the poor and ultra-rich, between capitalist owners and workers, is how do we end it? Yet in an economy where most people work long hours, are struggling to get by, and have deeply internalized the status quo, that question becomes: How do I get in?

That’s how a million-dollar jpeg of a digital rock turns out to make sense.

A couple of years ago, in the doldrums of the crypto bear market, after the prices of the two most adopted and largest cryptocurrencies, Bitcoin and Ethereum, imploded in 2018, I met a bubbly and talkative Uber driver. He was in his late 20s and had moved back in with his dad to improve his financial situation and was so bored of his sleepy Virginia suburb that sometimes, after a day of Uber driving, he would roam around Washington, DC, and then sleep in his car. (I suspected this was a bleak cover for being too exhausted to drive back home after a long day of driving. Drivers often say the grueling nature of gig workers requires sleeping in your car.) He said that he was routing much of his earnings to cryptocurrencies and using what was left of his whittled down free time to do extensive research on which ones to put his money into.

I winced when he told me that. After reaching an all time high at the end of 2017, the price of Ethereum, Bitcoin, and every other adjacent crypto token tanked, wiping out masses of amateur traders and speculators who jumped in, hoping to make life-changing money. Americans alone lost a collective $1.7 billion trading Bitcoin in 2018. Major news outlets ran stories about guys like Sean Russell, who effectively torched his $120,000 life savings by putting it all into Bitcoin in November 2017, only to lose 96 percent of his initial investment months later. In 2019, the public consensus was that putting money into crypto was a fool’s errand.

But then I thought about it for a second. Around half of Uber drivers make below their state’s minimum wage (which annualized comes out to not much higher than the federal poverty line), and most aren’t earning much more than that. If this guy wanted a way out of his potentially sub-$20,000-a-year earnings, he was going to have to get more out of his workday than his already lengthy work schedule. Rich people do this all the time. In the parlance of the personal-finance bible Rich Dad, Poor Dad, “They make money work for them.” Through a Rube Goldberg assemblage of stocks, real estate, and other “assets,” money compounds itself.

Uber drivers generally don’t have a lot of spare cash to throw around for investing, and even if you’re making the S&P 500 10 percent average annual return on your investments, that doesn’t add up to very much if your principal and contributions aren’t very big. In that context, trying to make it in crypto, where if you get lucky your principal investment could multiply 10, 50, or even 100 times in a few years, doesn’t seem like the dumbest thing in the world. And if he lost it all, his life wouldn’t be that much different from where it was then.

If you want more money, a higher wage isn’t going to cut it. You also need to monetize your remaining waking hours outside of work. You need to keep earning money 24 hours a day. This shift has infected everything from the type of college people go to (one that is sure to have a high ROI), to the degree that they pick (a business one increasingly) in the hopes of getting the highest paying job possible. Hobbies are side hustles. Your time is an investment. Have you checked your 401(k)? Hustle is a way of life. Those with enough assets can afford to opt out. But a lot of us have become a tiny businesses, man.

The theorist Wendy Brown astutely observed in her 2015 book, Undoing the Demos: Neoliberalism’s Stealth Revolution, that now people “are construed on the model of the contemporary firm,” meaning that people are “expected to comport themselves in ways that maximize their capital value in the present and enhance their future value.” Many of us are forced to become as valuable as we can, thereby creating the most human capital possible. And as firms have moved from producing goods and services to becoming more lucrative through finance, the tiny businesses (us) have started to follow suit.

The rich have figured this out. In the past decade, according to Justin Farrell’s Billionaire Wilderness, the number of ultra-wealthy (people with at least a $30 million net worth) have grown rapidly at a rate of almost 10 percent a year with most of the new entrants minting their status through finance, investments, and banking work. According to 2017 analysis by the data firm Wealth-X a clear plurality (14.5 percent) of the ultra-rich attained their wealth in finance, banking, and investments. Meanwhile, the financial situation has more or less remained stagnant for most other people, while things keep getting more expensive.

Why is $SHIB surging so hard this year?

I think these three charts tell the whole story. pic.twitter.com/6Cirp7Gf0w

— Joe Weisenthal (@TheStalwart) October 25, 2021

When the people making all the money are bankers, venture capitalists, angel investors, private equity principals, and hedge fund managers, and you want to make money too, then why wouldn’t you emulate them?

Up until lately, you really couldn’t. But with the advent of options trading on fee-free platforms like Robinhood you can pull off bootlegged versions of the absurd trades that hedge fund king Ray Dalio and his gang over at Bridgewater Associates are doing. You used to only be able to be a seed investor in technology companies if you were an accredited investor (a fancy way of saying someone has a million-plus dollars). In cryptomarkets, you can run your own mini-venture capital operation by throwing money into early-stage projects with much less.

The GameStop stock run up that started earlier this year is maybe the most explicit example of the masses acting like financiers. Reddit traders on r/WallStreetBets didn’t come up with the idea to invest in GameStop on their own, they took it from Michael Burry, the hedge fund manager who predicted the 2008 housing crisis and was portrayed by Christian Bale in The Big Short. With their attempted short squeeze that helped produce a massive run-up, r/WallStreetBets took it further than Burry ever intended to, but the so-called populist finance move just started with (admittedly skilled) amateurs just doing what a hedge fund manager was doing.

As economic damage has trickled down from the decisions of high finance to middle and lower classes, ironically so have investment theories. The retail investor masses took the ideology of Andreessen Horowitz and Paul Singer—and now they want the returns, too.

In 2017, Brian Krogsgard had a stable, good job as a developer for a trade publication in Alabama when he realized if he wanted to ever stop working he would need a fortress of money around him. “I long had this mentality of putting 10 percent or 15 percent of my income away for retirement,” he told me. But “I was looking at the numbers one day and I realized that I needed need to put a lot more money in.” His parents only started saving relatively late, and imparted the financial lessons they were learning onto him in his childhood. Krogsgard wanted another life.

Soon after, he started putting money into Bitcoin and Ethereum. Now, he is singularly focused on it. He splits his time between managing his portfolio, co-hosting a Twitch show/podcast “UpOnlyTV,” and running a crypto-analysis firm, Flip Metrics.

The old models can work for some people—if they’re lucky. It’s possible to maybe retire comfortably by steadily accruing S&P 500 tracking ETFs. But that’s only a viable strategy if you don’t get laid off the next time the economy gets run into the ground and are forced to sell what you have at the nadir of the market. Or you could try to buy Dogecoin, participate in the next GameStop, faux-arbitrage Ethereum, buy a pixelated CryptoPunk (and flip it for multiple times over what you paid for it). Your savings could all go to zero, but that could have happened anyway with a single car accident, terminal illness diagnosis, or if your pipes burst in a freak ice storm. Or maybe your savings weren’t that far from zero anyway. Besides, what’s potentially losing a few thousand dollars on a risky investment compared to $70,000 of student debt, with no guarantee of a job after you graduate? People trying to shoddily arbitrage their future is just the next logical step in an economy in which every bit of your time needs to be monetized to come anywhere close to achieving stability anyway.

The truth is people need money badly and have few ways to get it. In a moment “marked by widening inequality and underemployment, ‘money,’ feels at once deadly serious and stupidly silly,” as Max Read succinctly put it in an essay for New York. “The pandemic economy isn’t an anomaly but a heightened version of one possible future: a world where money is abundant but safe long-term investments are rare and where ‘getting rich quick’ is less an American pathology and more the best bet for a stable life.” The side hustles, as it turns out, haven’t been working.

That’s true not just because opportunities for a stable income are drying up but because now, in the US, unless you are solidly wealthy or proximate to generous people who are, you are always one emergency from financial ruin—if you’re not already in it. What’s the point of being middle class if it can all still go south, no matter how responsible you are? Eventually, just being fabulously wealthy becomes the new standard of financial responsibility.

The pseudonymous crypto-influencer and investor DeFiGod1 put it in more concise terms to his followers on Twitter: “Middle class is getting wiped out. I hope you make it anon.”

“As long as job precarity is the case, people do what they can to live above that,” explained Rohan Grey, an assistant professor of law at Willamette University, who keeps a critical eye on crypto. “And the only way to do that is to get a good job, and we don’t have a system right now where everyone can have that.”

We certainly do not have that system—a point that’s not always acknowledged in critiques of cryptocurrencies and NFTs. Many of its biggest detractors are appalled at some segments of the cryptocurrency community’s aim of supplanting central banks and government monetary, financial, and economic policy. Creating technologies to bypass functions of democratic governments is dangerous. But people have good reason for being thoroughly frustrated at central banks and politicians, too.

Obama and Congress’ 2009 stimulus package saved the financial sector while driving the economy off a cliff for many others. Even though they eventually capitulated, Republican lawmakers recently had no problem flirting with not raising the debt ceiling and letting the country default, something that would have likely sent the entire American economy into a devastating tailspin. And while many of the regulations set in place do protect small-time investors, some reinforce inequities. Retail investors can’t touch sometimes lucrative private equity angel investments, because of accredited investor regulations, but as Krogsgard points out “they can go to Robinhood and put in bad call options that could easily take their net worth to zero.”

The proactive options regulators suggest don’t make sense for this economy either. In a video to college students and graduates, Securities and Exchange Commission Chair Gary Gensler suggested saving $5 a week. You’d have “$135,000 plus saved by the time of retirement at 65,” Gensler said—as though this is impressive. Given that the average student loan debt is about $3o,000, you can knock off that much from the $135,000. If inflation stays at its current 2.1 percent average of the last two decades, $135,000 then will be around $55,000 of today’s money. It’s not nothing, but probably wouldn’t go very far in retirement.

“People can obviously see the impracticality of those kinds of statements,” Krogsgard said of Gensler’s advice. “Most people live month to month. If you do, the goal of retirement can be impossible unless you put your money into a lotto ticket. I think that leads people to meme stocks and dog coins.”

Even though they stand to potentially get screwed in markets, retail investors have realized that they’re screwed if they don’t invest either. “People my age and older look at Robinhood, crypto, etc. with some disdain. They complain about ‘the financialization of everything,” Mat Dryhurst, an artist, researcher and co-host of the technology and art-focused podcast Interdependence, told me. “But I’ll talk to the 20-year-old students that I teach at NYU, who grew up with Instagram, and they look at me like ‘where the fuck have you been?’”

Their entire lives have already been metricized on Facebook, Instagram, Snapchat, Twitter, and the like, Dryhurst explained. To them, their portfolio value on Robinhood is just one more number, except it’s one that has a much more tangible impact on their lives.

“If you are 20 now, unless you were very fortunate, you grew up in post-2008 conditions, have scarce professional opportunities outside of the self-promotion platform economy, and ecological consequences looming before you,” Dryhurst explained. “So, the idea of access to direct investment opportunities is naturally very enticing. Slow and steady investment lore already seems outmoded to people of my generation when stable employment is becoming rarer. To them, it must seem supremely alien.”

All of this isn’t to mistake trying to find a path to financial stability through options trading or crypto investing as a good idea. It’s not for most people, even if it’s arguably rational. Nor is finance ever a useful solution for ameliorating social ills. For some like Krogsgard, risky, speculative bets will work out, but some sucker has to get stuck holding the bag for the whole thing to work. As David Roth puts it in an essay about crypto for Defector, “There is the invitation to join an expert elite and get the same incredible deal they’re getting…The most obvious aspirational aspect of all this is the chance to get rich, but there is also a strong associational benefit to pulling yourself up out of the broader starving chaos of hopeless marks.”

Just like hedge funds and venture capitalists, everyone trying to buy low and sell high are competitors trying to screw each other over. And especially in high finance, not everyone wins—especially the less powerful.

As Grey told me, “[Financial institutions] want to make less sophisticated investors feel like they’re on equal footing. And that’s not ever true.” Robinhood, he pointed out, famously sells its order books to Citadel Securities so that institutional investors always know what Robinhood traders are doing before their trades are even executed, and can always beat them.

In crypto markets, by design, participants are less centralized, and are more diverse in their motivations and levels of altruism. At least a few deep-pocketed whales have manipulated markets. For example, experts suspect that the prices of NFT (crypto-based digital art) have been partially run up by washtrading, in which traders anonymously buy digital art from themselves at higher prices to make it look like buyers are willing to pay more than they actually are. The whales know what’s happening, while smaller moneyed investors get jerked around. Yet, the small fish keep coming in.

It’s symbolic, but the continued financial infection of language suggests that the trend isn’t stopping. As “ROI” and “value-add” have become staples, new financial words are starting to take hold. People increasingly aren’t optimistic about something, they’re “bullish”—Wall Street slang for markets going up. There are terms on the horizon too that are poised to come out of the crypto boom. In crypto-following subcultures, “alpha,” a specific finance term indicating an investment’s performance over a benchmark like the S&P 500, has become extrapolated into a ubiquitous slang word that’s used to refer to anything vaguely insightful or valuable. Tips on potentially good investments are considered “good alpha” but also so are books, smart ways of thinking, and healthy lifestyle philosophies.

“Investing has become our language for all kinds of things. Including consumption. We talk about ‘I think I’m going to invest in a good pair of hiking boots’ instead of just saying ‘I’m going to ‘buy them,’” Brown elaborated to me over the phone. Words like “invest” aren’t being integrated into our life just because financial ideology is ubiquitous—our use of them reveals the moral value that we imbue onto finance.

“A sound investor is assumed to be a smart person. And a person who has knowledge of what’s a good investment and what’s a bad investment. Workers and consumers are seen as losers. Investors and speculators are winners,” she said.

The trend is starting to go in the opposite way, too. Non-finance slang is getting coopted into amateur investment trading. “YOLO,” popularized by Drake a few years ago, now can mean chasing big, quick gains in the market. “FOMOing in” means buying a quickly rising stock or crypto token in fear of missing out on it going up even more.

“Every human domain and endeavor, along with humans themselves,” is being transmogrified into “a specific image of the economic,” Brown noted in Undoing the Demos. By becoming miniature venture capitalists and hedge funds, we fulfill the logical progressions towards being homo oeconomicuses in which, as Brown puts it, “all conduct is economic conduct; all spheres of existence are framed and measured by economic terms and metrics, even when those spheres are not directly monetized.”

In this way, as finance becomes personal finance, personal finance just becomes the personal. Your Dogecoin or Ethereum Classic is just who you are too. And if you think that’s dumb, because Dogecoin and Ethereum Classic have no point beyond being vehicles by which people trying to get rich through, that is exactly the point.

Correction: A previous version of this article misstated the year the Obama administration’s stimulus package passed. It was 2009.

{kind=link}