It’s really hard to evaluate the effect of health coverage on health. Sure, you can compare groups with and without coverage, but they’re almost certain to be so different (in income, race, employment, age, etc) that it’s impossible to tease out the effect of health coverage itself. Ideally, you’d like to perform a randomly controlled trial where you take a single group and then randomly split it in half. One half gets coverage and the other doesn’t. Since the two groups are the same, it’s fairly straightforward to measure health differences and then calculate how they’re related to coverage.

Unfortunately, an RCT is all but impossible in this arena. How do you randomly deny health coverage to half a group, after all? It’s basically only been done once, when Oregon conducted a lottery to decide who would qualify for Medicaid coverage from a group of people on a waiting list. The Oregon study was interesting, but the sample size was smallish and the results have been hard to quantify.

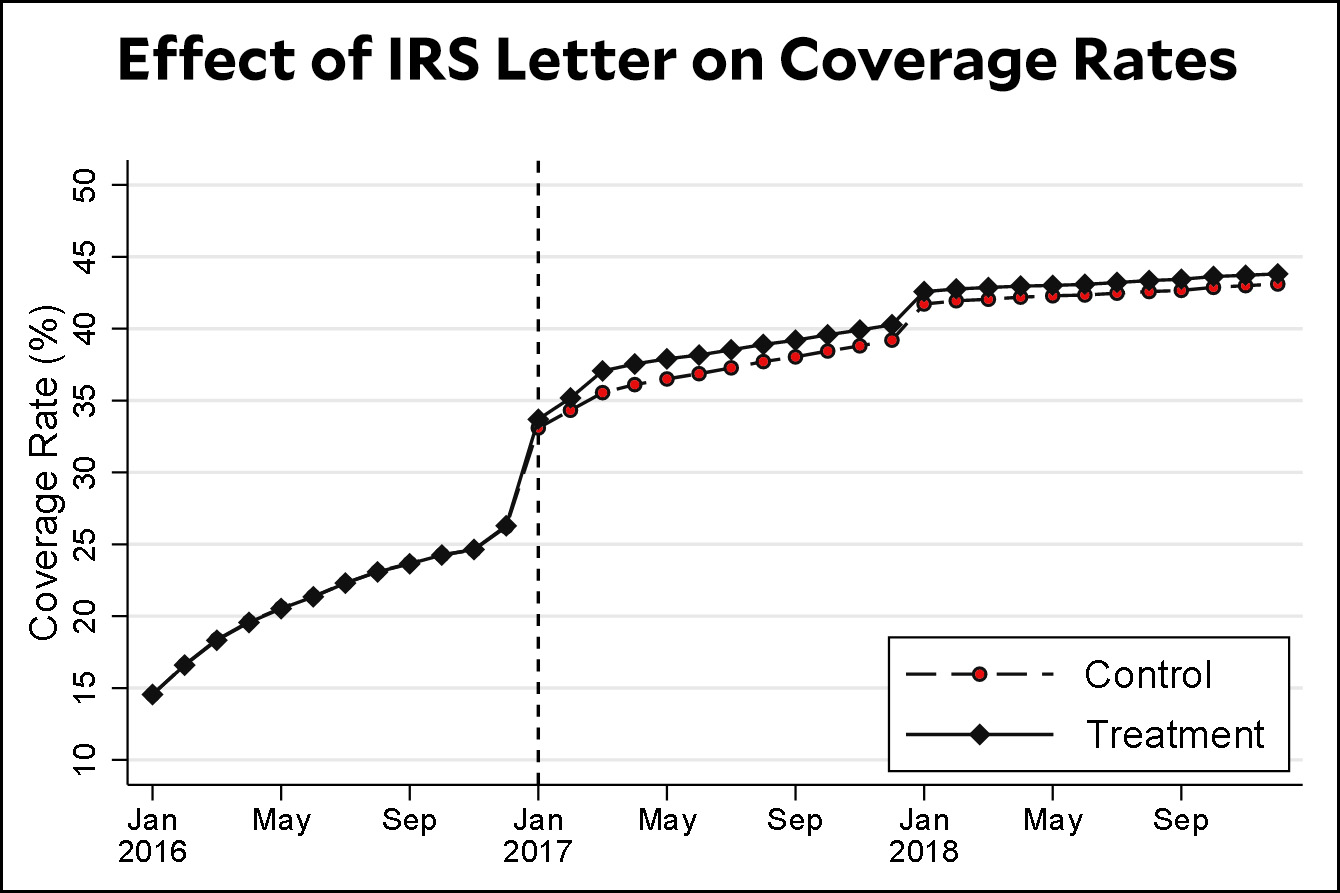

But now a team of researchers has conducted a different kind of RCT. In 2015 the IRS sent out a letter to people who paid a penalty for not having health insurance and provided them with information about the cost and availability of getting coverage via either Medicaid or one of the Obamacare exchanges. Millions of letters were sent out, but 14 percent of the group was randomly selected to not receive the letter. Here’s how that affected coverage in the following year:

The difference in takeup rates is about one percentage point. This may seem small, but when the test group is very large that’s plenty to deliver reliable results. Here’s what happened:

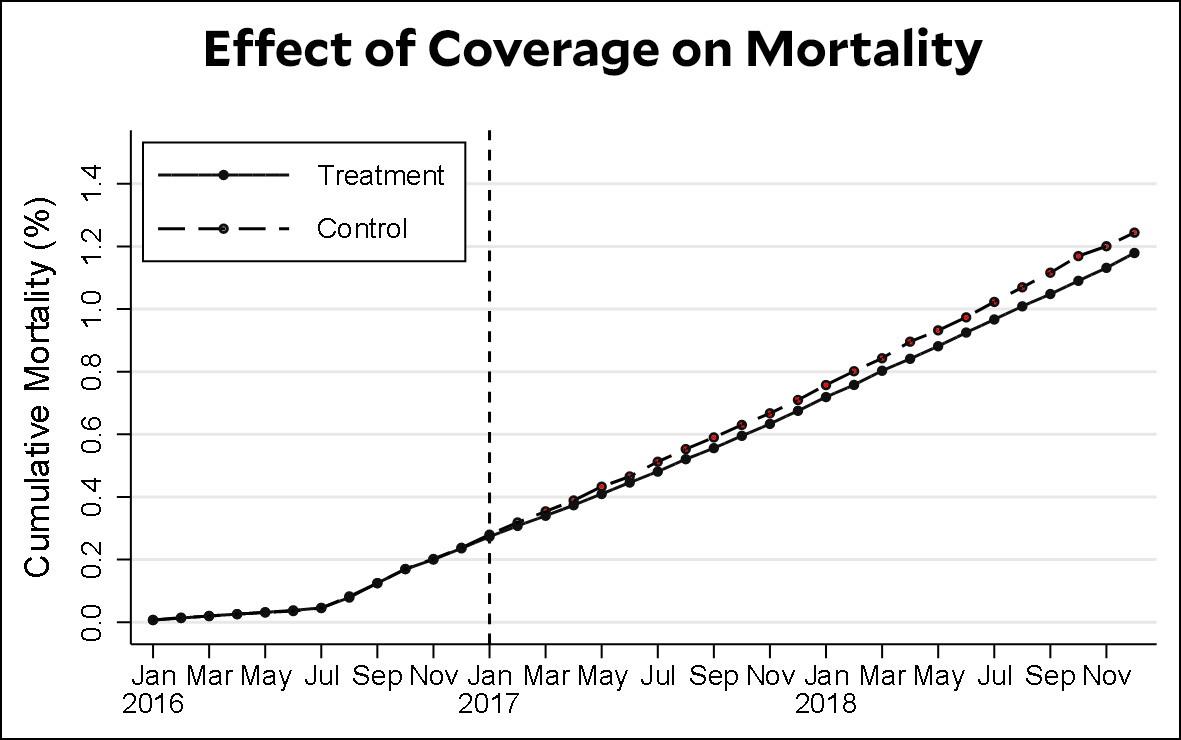

The control group, which had lower rates of coverage, also had higher mortality rates. The difference is small, about 0.05 percentage points, which is not surprising since the death rate for middle-aged people is pretty small to begin with (in fact, the mortality part of the study was limited to individuals aged 45-64, since younger age groups have virtually zero mortality). But again, given the large size of the test group, it’s quite possible to draw conclusions from this difference:

We found positive effects of the intervention on subsequent coverage enrollment decisions, particularly for taxpayers who were uninsured in the year prior to the intervention. We also found that the intervention reduced mortality among middle-aged adults in the subsequent two years, which we attribute to the additional coverage the intervention induced. Our findings thus provide strong empirical support, and the first experimental evidence, for the hypothesis that health insurance coverage reduces mortality.

I’ve argued for a long time that focusing too much on mortality is misguided. Not only are mortality differences small among the non-elderly to begin with, which makes it hard to study even under the best circumstances, but mortality is a tiny part of what health care is about. By far, the greatest effect of health care for most of us is simply to make us feel better. We get antidepressants. We get flu shots. We get CPAP machines. We get artificial knees and hips. We get asthma inhalers. Most of these things have either no effect on mortality or only a tiny effect. Nonetheless, we’re collectively willing to pay a lot of money for this care, and we lead far better lives because of it.

That said, it’s common sense that health coverage should also have some effect on mortality, and arguments to the contrary have always seemed a little silly to me. How could it not? That makes it nice to see experimental evidence confirming this.

As always, this is just a single study and it might turn out that there are flaws in its design. Still, it’s the first to make use of a truly large test group, one that’s big enough to pick up tiny differences. And those differences, it turns out, are real.