Flickr/Andres Rueda

First, happy Credit CARD Act day! As I wrote last week, the second phase of the Credit Card Accountability Responsibility and Disclosure Act of 2009 goes into effect today, cracking down on unfair and predatory practices like universal default and unfair interest rate hikes. You can read more about those changes here [PDF]. Sadly, banks are trying awfully hard to pass along the cost of new regulation to their customers. In my post from last week, I told how a Citi Card customer who contacted us here at MoJo could face a $60-a-year fee for—get this—not charging enough money to her card.

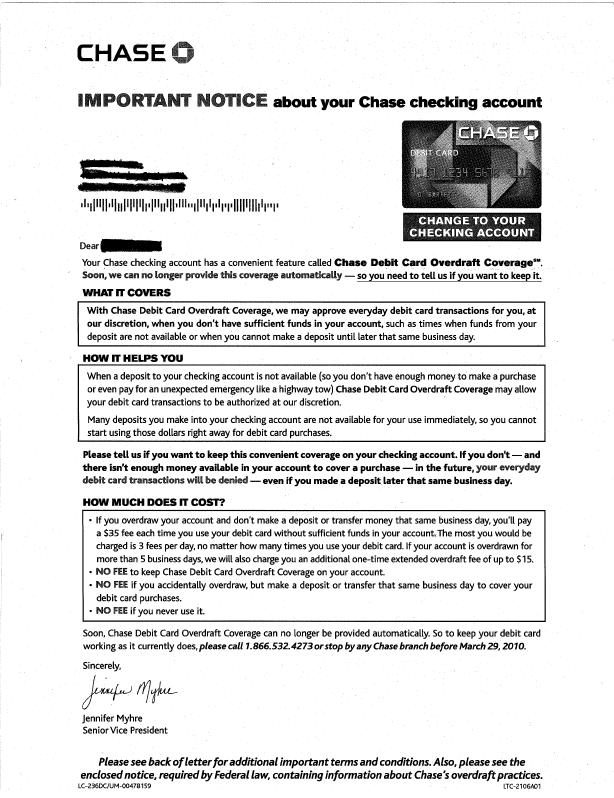

James Kwak, over at Baseline Scenario, heard from a reader with a similar story on how Chase is pleading with its customers keep their overdraft service which consumers can now opt out of thanks to the new legislation. Kwak, who posted Chase’s letter to its customer, wasn’t surprised:

There’s nothing particularly evil about this—banks will no longer be allowed to charge overdraft fees without your consent, and even I will concede that there are some people who might want this service, so now they have to ask for permission. Of course, it’s a pretty hard and misleading sell: they focus primarily on the issue of funds availability (deposits may not be available immediately), and they try to frighten you with “an unexpected emergency like a highway tow.” If you do get a letter like this and are not sure what it means, remember that the bank will not tell you when you are about to overdraw your account, and it will charge you $34 each time, even multiple times per day, no matter how small the overdraft.

I was interested to note that the bank doesn’t even promise that it will cover your overdraft—it says only that it may cover your overdraft, at its discretion. I suppose this makes sense, since they don’t want to cover an overdraft for $100,000, but couldn’t they guarantee it up to some fixed amount? I mean, if this service is supposed to give you peace of mind, how much peace of mind do you get when the bank reserves the right not to cover your overdrafts? [emphasis mine]

For all their convenience, overdrafts can be a nasty, unfair practice; if you calculate the APR from the average overdraft fee, it’s more than 10,000 percent. No matter how well Chase or any other bank cloaks the practice is corporatespeak, we’re all better off now with the chance to opt out of overdraft fees.

{kind=link}